Analysis

The 2026 Medicare Sticker Shock: Why Your COLA Raise Is Already Gone

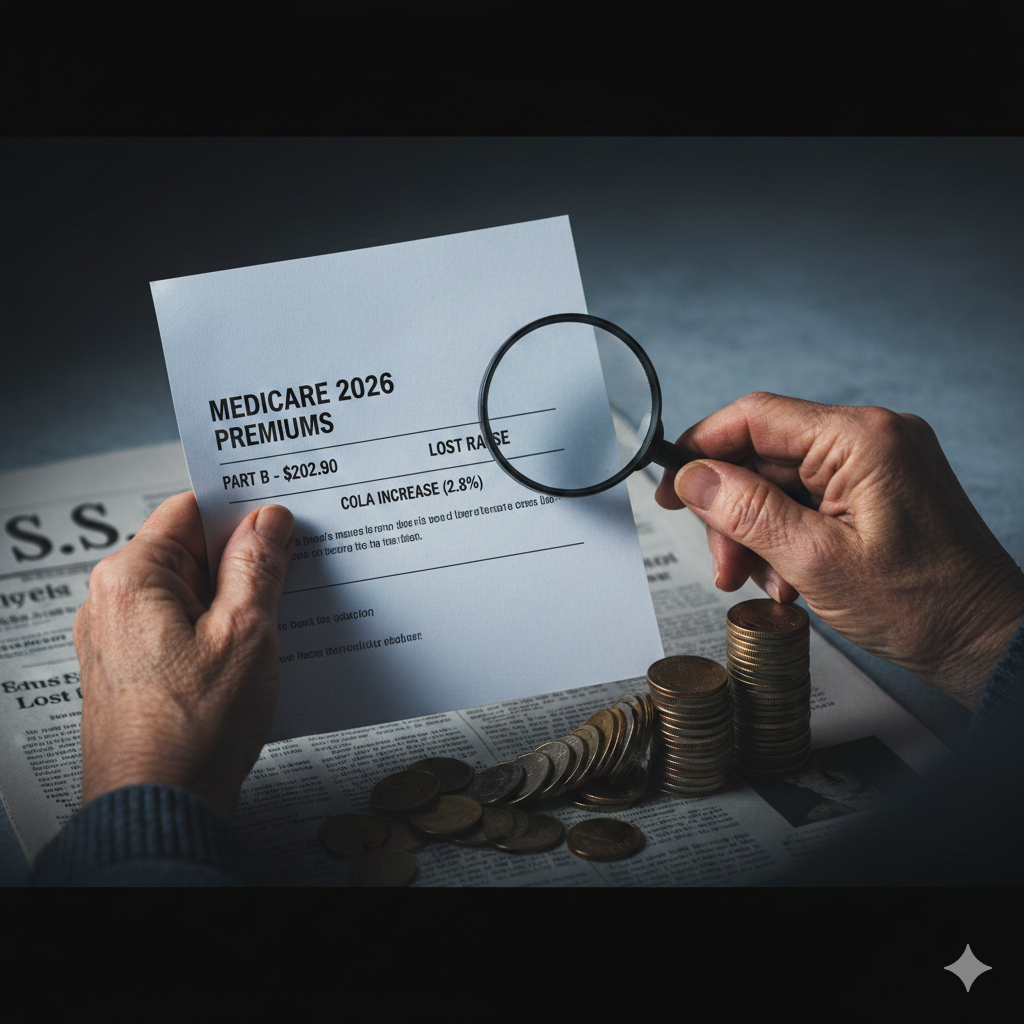

The Social Security Administration delivered the news retirees desperately wanted to hear: a 2.8% 2026 Social Security COLA increase, designed to shield fixed incomes from persistent inflation. For the average retiree, that translates to roughly a $56 per month increase.

Sounds good, right? Don’t deposit that phantom raise just yet.

As a senior healthcare policy analyst, I can tell you that the accompanying announcement from the Centers for Medicare & Medicaid Services (CMS) is the silent thief in the night. The sharp increase in Medicare 2026 premiums is poised to claw back nearly one-third of the entire COLA, leaving millions of seniors with little more than a nominal net increase—and, for some, no increase at all.

The illusion of a raise is quickly yielding to the reality of the healthcare squeeze.

Table of Contents

The Brutal Math: How the Premium Hike Neutralizes the COLA

The key numbers that matter most to retirees on Original Medicare are staggering.

- Old Standard Part B Premium (2025): $185.00

- New Standard Medicare Part B premium 2026: $202.90

- The Difference: An increase of $17.90 per month.

Since the Part B premium is automatically deducted from your Social Security check, this is an immediate, inescapable reduction to your net income.

| Calculation | Monthly Increase | Impact |

| Gross COLA Increase (Avg.) | ~$56.00 | The headline raise. |

| Less: Part B Premium Hike | -$17.90 | The mandatory deduction. |

| Net Gain (Avg.) | ~$38.10 | What’s left for food, gas, and utilities. |

That $17.90 hike consumes approximately 32% of the average retiree’s raise, bringing the effective COLA down from 2.8% to around 2.1%. After a year of intense inflation hitting food, fuel, and housing, this marginal net gain offers almost no genuine retiree inflation protection. It is the largest erosion of the COLA by Medicare premiums since 2017.

The Hidden Costs You Must Also Face

Beyond the standard premium, two other numbers underscore the rising financial pressure:

- Medicare Part B deductible increase: This is rising from $257 to $283. This is the amount you must pay out-of-pocket annually before Part B coverage kicks in.

- Part A Inpatient Deductible: This is also rising to over $1,736 per benefit period. A single, unexpected hospitalization could now cost hundreds of dollars more than it did in 2025.

For those with smaller Social Security checks, the “hold harmless” provision will thankfully prevent your net benefit from decreasing. However, it also means your check essentially won’t grow at all, leaving you with zero net benefit from the COLA to battle rising consumer prices.

📈 The Wealth Penalty: IRMAA Brackets 2026

The squeeze is exponentially tighter for affluent and upper-middle-class retirees who are subject to the Income-Related Monthly Adjustment Amount (IRMAA). This surcharge requires higher earners to pay a larger percentage of the Part B program cost.

The initial IRMAA trigger is now based on your 2024 tax filing.

- IRMAA Trigger 2026 (Single Filers): Modified Adjusted Gross Income (MAGI) > $109,000

- IRMAA Trigger 2026 (Joint Filers): MAGI > $218,000

The problem? Many retirees are only slightly above these thresholds, often due to a single, planned event like selling an appreciated asset or executing a small Roth conversion. Falling into that first IRMAA bracket can jump your total Part B monthly premium from $202.90 to $284.10 (and higher tiers escalate steeply from there), completely vaporizing the 2.8% COLA and potentially reducing your actual net monthly income.

Actionable Advice: Three Moves to Protect Your Income Now

The reality of these high Medicare deductible 2026 and premium costs demands a proactive financial stance. Here are three strategies to mitigate the damage:

1. Optimize Your Taxable Income (The IRMAA Strategy)

If you are close to an IRMAA threshold, work immediately with your tax advisor to manage your 2026 IRMAA brackets exposure.

- Qualified Charitable Distributions (QCDs): If you are 70.5 or older, use QCDs from your IRA to satisfy your Required Minimum Distribution (RMD). This lowers your MAGI without generating taxable income.

- Roth Conversions: Strategically time any Roth conversions to stay under the IRMAA limit. A large conversion this year could cost you thousands in surcharges two years from now.

2. Review Your Part D and Medicare Advantage Options

Since this is Open Enrollment Season, don’t default to your old plan.

- Part D Surcharges: IRMAA also applies to Part D prescription drug coverage. Review your Part D plan’s premium and its coverage of your specific medications.

- Medicare Advantage: While not for everyone, many MA plans offer $0 Part B premiums and incorporate Part D coverage, offering a way to avoid the direct Part B premium hike—though you must weigh network restrictions and out-of-pocket limits.

3. File an IRMAA Appeal (The SSA-44)

Did a life-changing event (e.g., stopping work, reduction in work hours, divorce, death of a spouse) significantly reduce your income since 2024? If so, you can file a Form SSA-44 with Social Security to appeal the IRMAA determination based on your current reduced income, potentially lowering your premium tier immediately.

The 2.8% COLA was supposed to be a lifeline against inflation. For millions of American seniors, it will instead be a transfer payment to cover soaring healthcare costs. Planning now is the only way to ensure the net number on your Social Security check is maximized.

Discover more from The Monitor

Subscribe to get the latest posts sent to your email.

Over 4 million Myanmar refugees in Thailand face police extortion, aid cuts, and legal limbo in 2026. A landmark work permit policy offers hope — but millions of undocumented Burmese migrants remain dangerously exposed. A premium investigation.

Table of Contents

The Street Becomes a Trap

Every morning, Naw Paw — a 34-year-old Karen woman who fled the Irrawaddy Delta shortly after Myanmar’s military coup in February 2021 — maps her walk to the garment workshop in Mae Sot with a single overriding thought: which roads have police checkpoints today. She knows most of the officers by the shifts they work. She knows which ones accept 200 baht, which ones demand 500. She has paid bribes she cannot afford more times than she can count.

“I never feel safe,” she told a rights researcher earlier this year. “Even when nothing is happening, I am afraid. I am always afraid.”

Naw Paw is one of an estimated 4 million Myanmar nationals now living in Thailand — the largest single-nationality migrant population in any Southeast Asian country. She is also among the roughly 1.7 million of them who are undocumented, meaning she exists in a legal void: unable to regularize her status, barred from formal work, excluded from the Thai government’s own refugee protection mechanisms, and left almost entirely vulnerable to the whims of local police. In border towns like Mae Sot, the informal extortion of undocumented Myanmar nationals has become so normalized that locals use a darkly revealing phrase to describe them: walking ATMs.

Four years after the generals in Naypyidaw seized power and set their country ablaze, the humanitarian fallout has reached a scale that Thailand — and the international community — can no longer manage by looking away.

Four Million People, and Counting

The numbers alone are staggering. The International Organization for Migration (IOM) estimates that more than 4 million Myanmar nationals currently reside in Thailand. Of those, nearly half — approximately 1.7 million — are undocumented, according to the Human Rights Watch July 2025 report, which documents their daily exposure to harassment, arrest, and forced deportation.

A further 90,000 mostly Karen and Karenni refugees live in nine government-administered camps strung along the Thai-Myanmar border — settlements that have existed since the 1980s and whose residents, in some cases, have now spent their entire lives inside the wire. The UNHCR registers more than 80,000 of these camp residents, along with roughly 5,000 urban asylum-seekers from more than 40 countries.

The scale of this population represents, in microcosm, everything that has gone wrong in Myanmar since February 2021: a military junta that has carried out crimes against humanity, a collapsing economy, fractured healthcare and education systems, and a countryside scorched by conflict. People are not crossing the Moei River into Thailand because they want to; they are crossing because staying has become unbearable.

What awaits them on the other side, however, is a protection system riddled with gaps — and, for far too many, a second layer of suffering.

“Walking ATMs”: The Extortion Economy

Thailand is not a signatory to the 1951 Refugee Convention. It has no domestic refugee law applicable to all nationalities. Its 2023 National Screening Mechanism — hailed by Bangkok as a reform — was designed with an exemption so large it swallows the mechanism whole: it explicitly excludes migrant workers from Myanmar, Cambodia, and Laos. Since the overwhelming majority of Myanmar nationals enter Thailand through migrant worker channels, they fall entirely outside the system’s protection.

The result is a population kept in permanent legal precarity — and Thai police have learned to profit from it.

HRW’s 48-page report, based on in-person interviews with 30 Myanmar nationals in Thailand in February 2025, documents a pattern of police stops, interrogations, and demands for bribes carried out with the implicit threat of arrest and detention. The phrase “walking ATMs” — used by residents of Mae Sot — captures not just the individual transactions but the systemic architecture: vulnerability is the product, and those who hold legal power over undocumented migrants are its sellers.

Many Myanmar nationals rely on brokers to navigate the “pink card” system — officially the Non-Thai Identification Card — which facilitates legal residence and employment. But the brokers charge exorbitant fees, the cards are often linked to fictitious employers, and a regularization window opened by the Thai Cabinet in September 2024 (extended in February 2025) has left most applicants in a renewal limbo that offers documentation but not genuine security.

“After fleeing conflict, persecution, and deprivation, Myanmar nationals need protection in Thailand,” said Nadia Hardman, refugee and migrant rights researcher at Human Rights Watch. “Instead, Thailand denies them secure legal status, and its authorities use that vulnerability to exploit and extort them.”

Urban undocumented Burmese migrants self-restrict their movement so severely that many avoid seeking medical care for serious conditions, pulling their children out of school at the first sign of increased police activity. The fear of deportation — back to a country under military rule, back to forced conscription, back to airstrikes and burning villages — operates as a form of continuous psychological violence.

The Camps: Aid Collapse and a Generation in Limbo

If conditions for undocumented Myanmar migrants outside the camps are defined by fear and exploitation, conditions inside the nine border camps have been defined, since 2025, by hunger.

The Trump administration’s dismantling of USAID in early 2025 triggered a cascade of funding failures that landed hardest on the most isolated. The Border Consortium (TBC), which had provided food assistance to camp residents for decades, terminated standard food aid for over 80 percent of families on July 31, 2025, after US funding was cut. Primary healthcare services from the International Rescue Committee followed. As HRW reported in August 2025, the monthly food allowance for adults had already been cut to just 77 baht — roughly US$2.30 — before the complete termination of food aid.

“In the past, we had enough rations,” one 34-year-old camp resident told HRW. “But the funding’s been cut bit by bit. The cash decreased and prices went up. I get 77 baht a month, but you can’t buy anything with that.”

Between 2022 and 2024, chronic malnutrition among children under five in the camps had already increased for the first time in at least a decade. The aid collapse accelerated what was already a slow-moving emergency.

For the youngest residents — who make up nearly 30 percent of the camp population — the education system has been crumbling in parallel. In January 2026, Save the Children warned that access to education in the border camps had reached “breaking point,” with student numbers rising 33 percent — from roughly 18,000 in 2020 to 24,000 in 2025 — even as funding collapsed. Classrooms of up to 60 students share frayed textbooks. Teachers face legal constraints that prevent them from holding Thai teaching licenses. Many learning centres operate on rented land, with no security of tenure.

The human cost is concentrated in a generation that has known nothing but the camps. One 25-year-old named Jornay, born in Mae La and interviewed by Save the Children, put it with quiet devastation: “I was educated in the camps, but our education was not recognized, so after we graduate, we don’t have jobs.”

Mae La, the oldest and largest of the nine camps — a dense settlement of wooden houses on the hills near Mae Sot, carved through with narrow muddy roads — has residents who have been there since the 1980s. Hope of resettlement abroad, always fragile, largely evaporated after the Trump administration halted a new resettlement program in early 2025, forcing two dozen refugees back to Umpiem Mai camp when their flight was cancelled in February.

“Having the card means we can’t go anywhere, we can’t apply for jobs, we can’t study,” a teacher who had spent 17 years in the camps told HRW. “We have no future, no opportunities. Our lives are in limbo.”

A Landmark Step — and Its Limits

In this landscape of compounding crises, August 26, 2025 marked a genuine departure. Thailand’s Cabinet approved a landmark policy allowing Myanmar refugees living in the nine border camps to work legally outside for the first time in decades. It is a significant concession — driven, in part, by economic necessity.

The timing was not coincidental. An escalating border dispute with Cambodia in 2025 prompted the return of over 780,000 Cambodian migrant workers to their home country. Since Cambodians had represented approximately 12 percent of the Thai workforce, entire industries — agriculture, manufacturing, construction, food processing — found themselves facing acute labor shortages. With an aging Thai population and a structural deficit of low-wage workers, the refugee camps along the Myanmar border began to look less like a humanitarian problem and more like an untapped labor reservoir.

As HRW noted, the new permits will be available to approximately 80,000 camp refugees registered with the Thai government, of whom an estimated 42,000 are of working age. Refugees must apply for permission to leave the camps and for work permits valid up to one year, tied to employer sponsorship. It is a pilot program — cautious, conditional, and heavily mediated by bureaucratic process.

“As young people, we want to make a living, we want to use our knowledge and skills,” one refugee told HRW. “If there’s any chance for us to leave the camp to work, to get a job and provide for our families, I would take it.”

UNHCR welcomed the Cabinet resolution as a meaningful step toward refugee self-reliance. For rights advocates, the challenge now is ensuring the application process remains free, transparent, and insulated from the broker networks and extortion dynamics that plague the broader migrant worker system. Every previous Thai regularization scheme has created new opportunities for intermediaries to extract fees from desperate people.

But even if the permit scheme functions flawlessly, its scope exposes the deeper problem: it covers roughly 80,000 people. The other 3.9-plus million Myanmar nationals in Thailand — the vast majority, living in urban areas, border towns, and informal settlements — remain entirely outside it.

The Urban Millions: Left Exposed

For undocumented Myanmar nationals in Bangkok, Chiang Mai, Samut Sakhon, and cities across Thailand, the August 2025 Cabinet resolution changed very little. They remain in legal limbo: too numerous to ignore, too undocumented to protect, and too economically essential to deport en masse — yet subjected to systematic harassment that extracts money while reinforcing their powerlessness.

Thailand’s structural reliance on Myanmar labor creates an inherent contradiction at the heart of its policy: the government needs these workers, but it has built no legitimate pathway for most of them to exist legally. The broker economy — which charges Myanmar nationals thousands of baht for pink cards linked to employers who may not exist — fills the gap, funneling money upward while leaving workers more exposed than before.

Human rights organizations, including UNHCR, have called for a temporary protection regime for all Myanmar nationals in Thailand — a status that would halt deportations, allow movement, and extend basic legal protections without requiring Thailand to adopt full refugee status determination procedures. Bangkok has not moved in that direction.

There is also a more sinister dimension: credible reports of junta informants operating within Myanmar migrant communities in Thailand, monitoring diaspora political organizing and reporting back to Naypyidaw. For those who fled specifically because of their political activity or ethnic identity, even the relative safety of Bangkok can feel provisional.

What Thailand Must Do — And Why It Should

The economic case for extending legal protection to Myanmar nationals in Thailand is not merely humane — it is hard-headed. Thailand faces a demographic crunch. Its workforce is aging rapidly. Industries that drive export revenue — including agriculture, seafood processing, and construction — are structurally dependent on low-wage migrant labor. A rights-respecting integration framework would not just alleviate suffering; it would stabilize a labor supply that the Thai economy cannot function without.

Rights groups and the UN have converged on a set of concrete demands:

- Introduce a temporary protection regime for all Myanmar nationals, halting deportations and extending legal status regardless of how people entered Thailand

- Expand the work permit program beyond camp residents to undocumented Myanmar nationals in urban areas

- Ratify the 1951 Refugee Convention, or at minimum adopt domestic legislation creating genuine asylum procedures applicable to all nationalities

- End police extortion through accountability mechanisms, independent monitoring, and criminal consequences for officers who exploit migrants

- Restore humanitarian funding for border camp services — food, healthcare, and education — through diversified donor commitments that reduce dependence on any single government

- Integrate camp schools into the Thai national education system so that children’s qualifications are recognized and pathways to the workforce open

The ASEAN dimension matters here too. Thailand is not alone in hosting Myanmar refugees — Malaysia, Indonesia, and India all carry portions of the load, and all face similar tensions between economic pragmatism and rights commitments. A regional framework for temporary protection, brokered through ASEAN mechanisms, would distribute pressure more equitably and reduce the incentive for any single host country to maintain exploitative conditions as a deterrent.

The international community, meanwhile, must recognize that the aid funding collapse of 2025 did not just harm individual refugees — it destabilized one of Southeast Asia’s most fragile border regions, creating conditions for trafficking, organized crime, and further political radicalization. Penny-pinching on humanitarian budgets in periods of great-power political realignment costs far more in the long run than the contributions foregone.

Conclusion: The Arithmetic of Exposure

The arithmetic of this crisis is brutal in its clarity. Thailand hosts more than 4 million people from Myanmar. Ninety thousand live in official camps that have just — tentatively, conditionally — been given the right to work. The other 3.9 million live in a system that is designed neither to protect them nor to acknowledge their presence with any dignity.

For Naw Paw, planning her route to work in Mae Sot around police checkpoints, the August 2025 Cabinet resolution is abstract comfort. She is not in a camp. She is not registered. She does not have a pink card linked to a real employer. She has what millions of Burmese refugees in Thailand have: a daily calculation of risks, a practiced ability to disappear, and the knowledge that if something goes wrong, the system will not save her.

Four years on from the coup, Thailand stands at a choice. It can continue managing Myanmar’s displaced millions through a combination of selective legalization, systematic exploitation, and willful blindness. Or it can build something that actually works — for refugees, for Thai industry, and for the region’s long-term stability. The landmark August 2025 work permit policy is a proof of concept. The question is whether Bangkok has the political will to scale it.

The answer matters to millions of people who are still running out of road.

Frequently Asked Questions (FAQ)

Q: How many Myanmar refugees are currently in Thailand as of 2026? According to IOM estimates, more than 4 million Myanmar nationals currently live in Thailand. Of these, approximately 90,000 reside in nine official border camps, while the vast majority — including an estimated 1.7 million who are undocumented — live and work across Thailand in legal limbo.

Q: Are Myanmar refugees in Thailand allowed to work legally? As of August 2025, Thailand’s Cabinet approved work permits for approximately 80,000 registered camp refugees — the first such authorization in decades. However, the estimated 3.9 million Myanmar nationals living outside official camps, including nearly 1.7 million undocumented individuals, remain excluded from legal employment pathways and are vulnerable to exploitation.

Q: Why are undocumented Myanmar migrants in Thailand called “walking ATMs”? The phrase, used by residents of Mae Sot on the Thai-Myanmar border, refers to the practice of Thai police extorting money from undocumented Myanmar nationals — stopping, interrogating, and demanding bribes under the threat of arrest and deportation. Human Rights Watch documented this systemic extortion pattern in its July 2025 report, “I’ll Never Feel Secure.”

Q: What has the US aid funding cut meant for Myanmar refugee camps in Thailand? The Trump administration’s dismantling of foreign assistance in 2025 led directly to the termination of standard food aid for over 80 percent of camp families by July 31, 2025, as well as the collapse of primary healthcare services. Monthly food allowances had already been slashed to approximately US$2.30 per adult before full termination. Save the Children separately reported in January 2026 that education in the camps had reached “breaking point” due to underfunding amid rising student numbers.

Sources

- Human Rights Watch — “I’ll Never Feel Secure”: Undocumented and Exploited Myanmar Nationals in Thailand (July 2025): https://www.hrw.org/report/2025/07/14/ill-never-feel-secure/undocumented-and-exploited-myanmar-nationals-in-thailand

- Human Rights Watch — Thailand Allows Myanmar Refugees in Camps to Work Legally (August 2025): https://www.hrw.org/news/2025/08/27/thailand-allows-myanmar-refugees-in-camps-to-work-legally

- Human Rights Watch — Thailand: Aid Cuts Put Myanmar Refugees at Grave Risk (August 2025): https://www.hrw.org/news/2025/08/11/thailand-aid-cuts-put-myanmar-refugees-at-grave-risk

- Save the Children — Education in Refugee Camps on Thailand-Myanmar Border Reaches ‘Breaking Point’ (January 2026): https://www.savethechildren.net/news/education-refugee-camps-thailand-myanmar-border-reaches-breaking-point-report

- UNHCR — Thailand Country Page: https://www.unhcr.org/us/where-we-work/countries/thailand

- Center for Global Development — A Breakthrough for Refugees’ Work Rights in Thailand and Malaysia?: https://www.cgdev.org/blog/breakthrough-refugees-work-rights-thailand-and-malaysia

- Reuters — Leaving Border Camps for Orchards: Myanmar Refugees Join Thai Workforce (November 2025): https://www.reuters.com/world/asia-pacific/leaving-border-camps-orchards-myanmar-refugees-join-thai-workforce-2025-11-19/

- The Guardian — Thailand to Let Myanmar Refugees Work Amid Aid Cuts and Labour Shortages (October 2025): https://www.theguardian.com/global-development/2025/oct/22/thailand-to-let-myanmar-refugees-work-aid-cuts-labour-shortages

Discover more from The Monitor

Subscribe to get the latest posts sent to your email.

Analysis

What Is the No Kings Protest? Inside Minnesota’s Historic 2026 Flagship Rally Against Authoritarianism

The flagship “No Kings” rally at the Minnesota State Capitol wrapped up around 5 p.m. Saturday, and organizers said more than 200,000 people came out for the anti-Trump rally in St. Paul. Star Tribune The crowd — pressed shoulder-to-shoulder across the Capitol lawn in a blustery late-March wind — had not gathered simply to protest a policy or a politician. They had come to answer a constitutional question that, in the view of those assembled, had grown uncomfortably urgent: does the United States have a king?

The “No Kings” protests have been organized to protest the second term of U.S. President Donald Trump, focusing on his allegedly fascist policies and statements about being a king. Encyclopedia Britannica The slogan is deliberately spare, historically grounded, and legally precise. “Trump wants to rule over us as a tyrant. But this is America, and power belongs to the people — not wannabe kings or their billionaire cronies,” according to the No Kings website. ABC10 The phrase encapsulates a year-long escalation of civic fury — born in the summer of 2025, sharpened by bloodshed in Minneapolis, and now, on March 28, 2026, arriving at what organizers are calling the largest single day of protest in American history.

Bruce Springsteen called Minnesota “an inspiration to the entire country” at the rally. “Your strength and your commitment told us that this is still America, and this reactionary nightmare and these invasions of American cities will not stand,” he said. CNN Then he played “Streets of Minneapolis” — a song he wrote in January, in grief and in anger — and 200,000 people sang along.

Table of Contents

The Roots of No Kings: From Flag Day 2025 to a National Movement

To understand what the No Kings protest means, you have to begin on June 14, 2025 — Flag Day, and Donald Trump’s 79th birthday — when the administration staged a military parade down Pennsylvania Avenue that critics widely characterized as a display of executive vanity unbefitting a republic.

Indivisible and a coalition of pro-democracy partner organizations announced the No Kings Nationwide Day of Defiance on Flag Day. “June 14th is also the U.S. Army’s birthday — a day that marks when Americans first organized to stand up to a king. Trump isn’t honoring that legacy. He’s hijacking it to celebrate himself,” the announcement read. Indivisible

The date of the No Kings protest was chosen to coincide with the U.S. Army 250th Anniversary Parade, which was also Trump’s 79th birthday, and which critics argued politicized the military and mimicked displays typically seen in authoritarian regimes. Wikipedia Trump had warned demonstrators: “For those people that want to protest, they’re going to be met with very big force.” The threat backfired. Five million demonstrators attended the first “No Kings” rallies on June 14, 2025. Encyclopedia Britannica

The October 18, 2025 protests took place in some 2,700 locations across the country. Organizers estimated that the protests drew nearly 7 million attendees — a figure that would make it one of the largest single-day protests in American history. Wikipedia The coalition had grown to include more than 200 organizations: Indivisible, the ACLU, the Democratic Socialists of America, the American Federation of Teachers, Common Defense, the Human Rights Campaign, Planned Parenthood, and many others. Wikipedia

Each iteration had expanded the movement’s geographic footprint. Organizers said two-thirds of RSVPs for the March 28 rallies came from outside major urban centers — including communities in conservative-leaning states like Idaho, Wyoming, Montana, Utah, South Dakota, and Louisiana. PBS No Kings was no longer a coastal phenomenon, if it ever was.

What Does “No Kings” Mean? The Constitutional and Historical Logic

The slogan is not metaphor. It is, in the strictest sense, constitutional argument.

The architects of the American republic were obsessed with the danger of monarchy. As Sen. Bernie Sanders told the St. Paul crowd: “In 1789, they said loudly and boldly to the world that in this new nation of America, we don’t want kings.” Minnesota Reformer He then read the opening phrase of the Declaration of Independence before adding: “Our message is exactly the same: No more kings. We will not allow this country to descend into authoritarianism or oligarchy. In America, we the people will rule.”

The movement’s organizers have constructed the phrase with care. It speaks simultaneously to Trump’s rhetoric — he has repeatedly tested the legal limits of executive authority and made comments his critics read as monarchical — and to the structural critique that his administration has sought to concentrate power in the executive branch at the expense of Congress, the courts, and the states. Organizers have described Trump’s actions as “more akin to those of a monarch than a democratically elected leader.” NBC News

In countries with constitutional monarchies, people call the protests “No Tyrants,” to avoid confusion with anti-monarchic movements. PBS The linguistic adaptability of the slogan — its ability to travel across political cultures — is part of what has given the movement its global reach.

Minnesota as Epicenter: Operation Metro Surge and Two American Deaths

Minnesota did not volunteer to become the moral center of American democratic resistance. That role was thrust upon it — at gunpoint.

Federal agents killed two civilian protesters during Operation Metro Surge: Renée Good and Alex Pretti, who were both U.S. citizens. The operation disrupted the economy and civil society of Minnesota, with schools transitioning to remote learning and immigration arrests disrupting everyday business activities. Wikipedia

Renée Nicole Macklin Good was a 37-year-old writer and poet who lived in Minneapolis with her partner and a six-year-old child. Wikipedia She was shot and killed on January 7 by an ICE agent while in her car. Alex Jeffrey Pretti, a 37-year-old intensive care nurse at a U.S. Department of Veterans Affairs hospital, was shot multiple times and killed by two Customs and Border Protection officers on January 24 in Minneapolis. He was filming law enforcement agents with his phone and had stepped between an agent and a woman the agent had pushed to the ground. Wikipedia

The Trump administration defended both shootings. Bystander video told a different story. In a poll published January 13, Quinnipiac University found that 82% of registered voters had seen video of the Good shooting. NBC News The footage spread rapidly, and what it appeared to show — a woman in a car, posed no lethal threat; a nurse attempting to protect a stranger — became the evidentiary core of a national reckoning.

On January 28, 2026, Minnesota chief U.S. District Judge Patrick Schiltz found that ICE violated at least 96 court orders in Minnesota since January 1, 2026. On February 3, Judge Jerry W. Blackwell said that the “overwhelming majority” of cases brought to him by ICE involved people lawfully present in the United States. Wikipedia

“The federal government has refused to cooperate with state law enforcement, which is unique, rare and simply cannot be tolerated,” Minnesota Attorney General Keith Ellison said. ProPublica Minnesota sued the Trump administration for access to evidence in the three shooting cases — a lawsuit that signals a constitutional confrontation over states’ rights and federal immunity that legal scholars say has no modern precedent.

Over 60 CEOs of Minnesota-based companies — including the heads of 3M, Cargill, Mayo Clinic, Target, Best Buy, UnitedHealth Group, and General Mills — signed an open letter calling for an “immediate de-escalation of tensions.” Wikipedia When corporate America speaks in that register, it is not sentiment. It is a balance-sheet judgment about risk.

March 28, 2026: The Flagship Rally in Detail

Three marches converged on the Minnesota State Capitol from different directions — from St. Paul College, from Harriet Island, from Western Sculpture Park — before joining on the Capitol lawn for a 2 p.m. rally.

Gov. Tim Walz took the stage dressed in flannel on a blustery day, armed with fierce rhetoric. He attacked President Trump and applauded Minnesotans for standing up to the administration during Operation Metro Surge. Minnesota Reformer Lt. Gov. Peggy Flanagan and Rep. Ilhan Omar also addressed the crowd.

Joan Baez and Maggie Rogers performed Bob Dylan’s “The Times They Are A-Changin'” to an estimated 200,000 people. Minnesota Reformer Jane Fonda and veteran labor leader Randi Weingarten — president of the American Federation of Teachers — also spoke. Weingarten declared: “Donald Trump may pretend that he’s not listening, but he can’t ignore the millions in the streets today.” PBS

Sanders addressed the killings of Good and Pretti directly: “When historians write about this dangerous moment in American history, when they write about courage and sacrifice, the people of Minnesota will deserve a special chapter.” Minnesota Reformer He also railed against the war in Iran, counting off what he described as estimated casualties among Americans, Iranians, Israelis, and Lebanese.

Protesters held up a massive sign on the Capitol steps that read: “We had whistles, they had guns. The revolution starts in Minneapolis.” PBS

Bob Meis, 68, a retired lawyer who moved to Minneapolis from Iowa six months ago, became emotional when he spoke to reporters. He said he was angry and worried about his grandson in the Marines who may be deployed to the war in Iran. “It helps knowing how many people are here. I wish there was more we could do,” he said. Minnesota Reformer Niizhoode DeNasha, an Iraq War veteran who stood near the front of the stage, said he came to “stand up for the Constitution. I enlisted 20 years ago and I really believe in it, and I think rights are being trampled.”

A Nation and a World in the Streets

Minnesota was the flagship, but the movement was everywhere.

Organizers called Saturday’s protests “the largest single-day nationwide demonstrations in U.S. history,” saying more than 8 million people participated across thousands of events. More than 3,300 events were registered across all 50 states. ABC10

About 40,000 people marched in San Diego, according to police. PBS In New York, Oscar-winning actor Robert De Niro called the president “an existential threat to our freedoms and security.” euronews In Washington, D.C., hundreds marched past the Lincoln Memorial into the National Mall. In Driggs, Idaho — a town of fewer than 2,000 people in a state Trump carried with 66% of the vote — protesters gathered with “No Kings” signs.

Rallies took place in Europe with around 20,000 people marching in cities including Amsterdam, Madrid, and Rome. In Paris, mostly Americans living in France, along with French labor unions and human rights organizations, gathered at the Bastille. In Rome, thousands marched against the U.S. and Israel’s strikes on Iran, also criticizing Prime Minister Giorgia Meloni. euronews In London, protesters held banners reading “Stop the far right” and “Stand up to racism.”

Demonstrations were also planned in more than a dozen other countries, from Europe to Latin America to Australia. PBS The global dimension of the protests is analytically significant. When allied democracies — not just civil society organizations, but ordinary citizens — take to the streets to express alarm about American governance, the signal to Washington’s diplomatic partners and to global markets is not negligible.

The Economic and Geopolitical Dimension

Protest movements are often analyzed in purely political terms. The No Kings movement demands a broader frame.

Trump launched a deeply unpopular war with Iran alongside Israel that has been raging for one month, killing more than 1,500 civilians in Iran and 13 U.S. service members, and having far-reaching negative impacts on the global economy. Time Americans are now facing skyrocketing gas prices and a flagging economy due to the war. CNN

The Department of Homeland Security has been shut down since February 14 amid a standoff between Democrats and Republicans over immigration enforcement, leading to hours-long security lines at airports struggling with a staffing shortage among TSA agents. Time

The cumulative effect on investor confidence and U.S. soft power is difficult to quantify but easy to observe. When more than 60 Minnesota-based corporate chiefs sign letters calling for federal de-escalation, when Italy expresses concern about ICE involvement in Olympic security arrangements, when European labor unions march under American protest banners — these are not merely cultural moments. They are data points in a global reassessment of the United States as a reliable partner and a stable investment environment.

As the November midterm elections loom and the president’s approval ratings sink below 40%, Republicans are in danger of losing control of both chambers of Congress. euronews The No Kings movement has been careful to maintain strategic ambiguity about electoral ambitions, describing itself as a civic movement rather than a partisan one. But the math is not subtle.

What Comes Next: The Future of No Kings

The movement has displayed two characteristics that distinguish durable civic coalitions from passing protests: geographic breadth and institutional density.

What began in 2025 as a single day of defiance has become a sustained national resistance, spreading from small towns to city centers and across every community determined to defend democracy. Mobilize With over 8 million people participating in 3,300 protests, organizers at Indivisible have already announced a mass call to discuss directing this power into sustained, strategic action against what they call “the fascist takeover” of government. Indivisible

The movement’s organizers have been explicit that they see street protest as only one instrument. Boycotts, electoral registration, congressional pressure campaigns, and legal action are all part of the toolkit. The Minnesota lawsuit over evidence in the Good and Pretti shootings is itself a form of organized resistance — methodical, procedural, and aimed directly at the accountability gap that has most inflamed public opinion.

Leah Greenberg of Indivisible framed the stakes plainly: “People are coming out in every state, in every county, collectively, and saying, ‘Enough.’ We are going to stand against illegal war abroad. We are going to stand against secret police at home.” Democracy Now!

The slogan “No Kings” is, at its core, not a statement about Donald Trump. It is a claim about the nature of American government — a reminder, addressed to the executive branch, to Congress, to the courts, and to the electorate, that sovereignty in the United States does not reside in any single person. Whether that reminder is sufficient to alter the trajectory of the current administration will be determined by events that Saturday’s enormous crowds cannot control: court rulings, election returns, the slow grind of public opinion against the administration’s shrinking approval numbers.

What the crowds in St. Paul demonstrated, with unmistakable force, is that the argument is very much alive. The constitutional republic has not yet conceded the point. As Springsteen held his guitar aloft on the Capitol steps and 200,000 people roared, that — for now — was enough.

FAQs (FREQUENTLY ASKED QUESTIONS)

1. What is the No Kings protest and what does No Kings mean?

The No Kings protest is a series of nationwide demonstrations organized by Indivisible and over 200 allied groups to oppose what organizers describe as authoritarian overreach by President Trump’s administration. The phrase “No Kings” derives from America’s founding rejection of monarchy and is used to argue that Trump’s claims of executive power are incompatible with constitutional governance.

2. What happened at the Minnesota No Kings protest on March 28, 2026?

The Minnesota No Kings rally at the St. Paul Capitol on March 28, 2026 drew an estimated 200,000 people in the largest single event of the movement’s third national day. Headliners included Bruce Springsteen, who performed “Streets of Minneapolis,” as well as Sen. Bernie Sanders, Joan Baez, Maggie Rogers, Jane Fonda, and Gov. Tim Walz.

3. Why is Minnesota hosting the flagship No Kings rally in 2026?

Minnesota was designated the flagship location because of Operation Metro Surge — a large-scale federal immigration enforcement operation beginning in December 2025 — and specifically because federal agents fatally shot two American citizens, Renée Good and Alex Pretti, in Minneapolis in January 2026, sparking national outrage and protests.

4. How big is the No Kings protest movement and how many people attended on March 28, 2026?

The No Kings movement has grown significantly with each iteration: roughly 5 million attended in June 2025, 7 million in October 2025, and organizers claimed over 8 million across more than 3,300 events on March 28, 2026 — potentially making it the largest single day of protest in American history.

5. Who are Renée Good and Alex Pretti, and why are they central to the No Kings protests?

Renée Good was a 37-year-old writer and mother fatally shot by an ICE agent in Minneapolis on January 7, 2026. Alex Pretti was a 37-year-old VA nurse shot and killed by CBP officers on January 24, 2026, while protesting Good’s death. Both were U.S. citizens. Their killings became the defining catalyst for the third No Kings Day, and Bruce Springsteen dedicated his “Streets of Minneapolis” performance to their memory.

Discover more from The Monitor

Subscribe to get the latest posts sent to your email.

Analysis

Singapore’s Bold Bid to Become Asia-Pacific’s Gold-Trading Powerhouse: Why the City-State Is Racing to Capture Bullion Liquidity and Central-Bank Vaults

When gold briefly touched US$5,600 per troy ounce earlier this year — a price that would have seemed fantastical a decade ago — it was not traders on the floor of the London Metal Exchange who were most animated. It was central bankers from Warsaw to Kuala Lumpur, family offices in Singapore and Abu Dhabi, and sovereign wealth funds quietly recalibrating their exposure to a metal that has become the defining safe-haven asset of a fractured geopolitical era.

Even after a sharp pullback triggered by the outbreak of conflict in the Middle East dragged prices to around US$4,430 per ounce by late March, the structural story remains emphatically intact: gold’s gravitational centre is shifting east. And Singapore, with its formidable financial architecture and a reputation for regulatory elegance, intends to plant its flag firmly at that new centre. On March 27, 2026, the Monetary Authority of Singapore (MAS) and the Singapore Bullion Market Association (SBMA) unveiled four strategic focus areas designed to transform the city-state into Asia-Pacific’s premier Singapore gold-trading hub. It is, in every sense, a declaration of intent.

Table of Contents

The Eastward Drift of Bullion Power

To understand the ambition, first understand the moment. The World Gold Council projects central banks globally will purchase approximately 850 tonnes of gold in 2026, sustaining what has become one of the most consequential structural shifts in reserve management since Bretton Woods. Central-bank buying in 2025 reached 863 tonnes — historically elevated and geographically widespread, spanning Poland, Kazakhstan, Brazil, Malaysia, and Indonesia. In Asia alone, new entrants to official gold accumulation emerge almost quarterly, motivated by a common logic: in a world of dollar weaponisation, sanctions risk, and mounting geopolitical entropy, gold is the only truly neutral reserve asset.

J.P. Morgan Global Research forecasts combined central bank and investor gold demand averaging some 585 tonnes per quarter in 2026, underpinning its projection that prices could approach US$5,000 per ounce by year-end. Meanwhile, the World Gold Council’s annual survey recorded the highest central bank intention to buy gold since the survey was first conducted in 2019.

The institutional demand is substantial on its own. But pair it with the explosive growth of Asian retail and family-office demand — bar and coin demand is forecast to exceed 1,200 tonnes globally in 2026 — and the market opportunity for a well-positioned regional hub becomes unmistakable. Singapore, which removed goods and services tax on investment-grade precious metals in 2012, has long been a magnet for bullion storage and retail investment. What it has lacked is the deep capital-market plumbing — the derivatives, clearing infrastructure, and sovereign-custodian credibility — that would allow it to punch at the weight of London or Zurich. The initiative announced on March 27 is designed to close that gap with surgical precision.

Four Pillars, One Strategic Vision

The key focus areas were developed by a Gold Market Development Working Group that MAS and SBMA established in January 2026, building on detailed discussions and studies with industry participants in 2025. The working group reads like a who’s who of global bullion banking: DBS, ICBC Standard Bank, JPMorgan Chase, UBS AG, United Overseas Bank, SGX Group, and the World Gold Council sit at its core, supported by vault operators including Brink’s, Loomis International, and Malca-Amit, alongside trading houses StoneX APAC and YLG Bullion Singapore.

The four focus areas are individually significant. Taken together, they constitute a comprehensive blueprint for building a Singapore bullion market with genuine global depth.

1. Capital-Market Products: Building the Price-Discovery Engine

The first pillar is the development of gold-related capital-market products to promote price discovery and build liquidity. This is arguably the most technically demanding of the four goals and, in the long run, the most consequential. London dominates global gold pricing precisely because it is where the world’s deepest pool of paper gold — forwards, OTC derivatives, leases — meets its deepest pool of physical metal. Singapore currently lacks this two-sided market.

What might such products look like? Singapore-listed gold ETFs with physical backing in local vaults, gold forwards priced off a Singapore benchmark, and gold-linked structured notes accessible to regional wealth managers are all credible candidates. The SGX Group’s involvement in the working group hints at the ambition: a futures contract priced off kilobar gold (the one-kilogram bar standard prevalent across Asian markets and an accepted COMEX delivery contract) could serve as a genuinely Asian benchmark, less exposed to the idiosyncrasies of London’s 400-troy-ounce large-bar convention.

Establishing a vibrant Asia gold trading liquidity pool in Singapore would also give Asian producers, refiners, and jewellers a local hedge that does not require them to transact through time zones that are awkward for the region — an enduring frustration with London’s primacy.

2. Vaulting Standards: The Architecture of Trust

The second focus area — establishing robust, internationally aligned vaulting and logistics standards — is less glamorous but no less critical. The London Bullion Market Association (LBMA), which sets global Good Delivery standards for gold bars, provides the template. Singapore already hosts internationally reputable vault operators, but the absence of a formalised, regulator-backed standards framework has historically created friction for institutional clients accustomed to the certainty of LBMA accreditation.

Closing this gap matters for a straightforward commercial reason: institutional gold trading at scale — whether by a sovereign wealth fund, a pension manager, or an international trading house — requires documented chain-of-custody assurance, insurance frameworks, and logistics protocols that meet international audit standards. Singapore’s aspiration to house central-bank bullion, in particular, makes this pillar foundational. No central bank will deposit reserves in a jurisdiction whose vaulting standards are ambiguous.

The presence of Metalor Technologies Singapore — one of the world’s premier precious-metals refiners — among the working group’s technical participants signals that Singapore intends to offer not merely storage but an integrated precious-metals ecosystem: refining, vaulting, trading, and settlement, all under one regulatory canopy.

3. A Clearing System for OTC Gold Settlement

The third focus area may be the most operationally complex: building a clearing system to support secure and efficient over-the-counter settlement for trading both large bars (the 400-troy-ounce London convention, approximately 12.4 kilograms) and kilobars (one kilogram, the Asian institutional standard) in Singapore. This is, effectively, the plumbing that turns a storage location into a trading hub.

Currently, significant OTC gold trades involving Asian counterparties are typically settled through London infrastructure or via bilateral arrangements that carry meaningful counterparty risk. A Singapore-based clearing facility — ideally with central-counterparty clearing to eliminate bilateral exposure — would reduce settlement risk, lower transaction costs, and allow the market to function across Asian time zones without dependence on Western intermediaries.

The group will help establish a clearing system to support secure and efficient over-the-counter settlements when large bar and kilobar gold is trading in Singapore. Large bars of gold, which weigh about 12.4 kilograms, are the preferred standard for institutional trading and settlement in the London market. Kilobar, which has a weight of one kilogram, is the preferred standard in Asian markets and is an accepted delivery contract for COMEX gold futures contracts in the US.

The Singapore gold clearing system 2026 initiative thus serves a dual purpose: it creates the infrastructure for efficient local settlement and positions Singapore as a natural location for gold trading during Asian hours — a gap that neither London nor New York can fill on their own.

4. Central-Bank Vaulting: The Sovereign Dimension

The fourth and arguably most geopolitically resonant focus area is MAS’s stated intention to explore providing vaulting services for foreign central banks and sovereign entities. The gold is understood to be stored in MAS-owned vaults. This is a genuinely significant departure from Singapore’s existing role in the bullion ecosystem — and a direct play for the most coveted and creditworthy clients in the gold market.

Singapore’s proposal could potentially attract nations that have challenged the status and credibility of historic hubs such as London and New York. A number of countries including Germany have repatriated gold for security reasons, and there have been similar moves from Poland, the Netherlands and Serbia.

MAS Deputy Chairman Chee Hong Tat — who is also Singapore’s minister for national development — framed the initiative with characteristic measured confidence. “We are working closely with the industry to see how we can position Singapore as a gold trading hub in Asia,” he told reporters. He emphasised that Singapore’s ambitions are anchored in long-term ecosystem-building, not short-term price speculation: “When it comes to investments, there will be ups and downs. If you look at what we are doing, we are not placing bets on whether the prices in the short term will go up or go down. What we are doing is to create the ecosystem for gold trading activity to be based out of Singapore.”

For emerging-market central banks in Southeast Asia, South Asia, and the Gulf — particularly those that have historically stored reserves in New York or London but now seek diversification — Singapore offers something qualitatively distinct: a neutral, politically stable, rule-of-law jurisdiction in their own time zone, operated by a regulator with an impeccable international reputation. In an era when reserve assets can be frozen by Western governments with a keystroke, that proposition carries weight that is difficult to overstate.

The Competitive Landscape: Singapore vs. Hong Kong, Dubai, and the West

No analysis of the Singapore vs Hong Kong gold hub rivalry is complete without acknowledging the scale of Hong Kong’s ambitions. Hong Kong signed a cooperation pact with the Shanghai Gold Exchange and reiterated a pledge to expand gold-storage capacity to 2,000 tons within three years. A public campaign unveiled this year promotes the special administrative region as a trading, financing and storage hub for gold, with a government-run clearing system slated to begin trials this year.

Hong Kong’s trump card is proximity to mainland China — the world’s largest consumer and one of its largest producers of gold. All Chinese gold imports flow through the Shanghai Gold Exchange (SGE), creating captive volumes that give Hong Kong structural advantages in physical metal flow. The SGE cooperation pact is designed to extend those flows offshore, creating a mechanism for international investors to access Chinese gold demand through a familiar common-law jurisdiction.

But the Hong Kong model has vulnerabilities that Singapore is quietly exploiting. First, Hong Kong’s geopolitical positioning has become complex since 2020, and a meaningful cohort of international investors and central bankers view its regulatory independence with greater scepticism than in previous decades. Second, the SGE partnership, while commercially powerful, tethers Hong Kong to Beijing’s preferences in ways that could constrain its appeal to the same sovereign clients both cities covet. Third, Hong Kong’s clearing system remains under development — still finalising details of its proposed clearing system, including the type of bars permitted for delivery and the currencies in which trade can be settled.

MAS Deputy Chairman Chee Hong Tat said there is likely room for more than one regional trading centre for gold as rising uncertainty gives more investors reason to pivot to the safe-haven asset. “I think the space is big enough for us to coexist and for both cities to be able to grow our respective services,” said Chee. “There are some overlaps in the clients that we serve and the market segments that we target, but it’s also not completely identical.”

That diplomacy is appropriate. But the reality is that for central banks outside China’s sphere of influence — those in Southeast Asia, South Asia, the Middle East, and parts of Africa and Latin America that are actively diversifying reserve locations — Singapore and Hong Kong are not complementary; they are alternatives. Singapore’s pitch to this cohort rests on three durable advantages: political neutrality, regulatory credibility, and a track record of building world-class financial infrastructure without the complications of a major superpower’s hand on the tiller.

Dubai, the other significant rival for Asia-Pacific gold trading hub status, has carved out a genuine niche in physical gold — particularly for African production flowing towards Asian consumption. But its regulatory ecosystem for capital-market products is still maturing, and it lacks Singapore’s bench strength in institutional banking, derivatives, and financial technology.

London, the global benchmark, faces a different kind of threat: relevance drift. The post-Brexit fragmentation of European financial markets, combined with growing Asian dissatisfaction with a pricing benchmark set entirely outside their time zone, creates structural demand for a credible Asian alternative. Singapore is the only candidate with the institutional depth to satisfy that demand comprehensively.

The Economic Case: Jobs, Revenue, and Financial Resilience

Singapore’s gold-hub ambitions are not merely about prestige. The economic dividend from establishing the city-state as a genuine Singapore bullion market centre is measurable and meaningful. MAS and SBMA noted: “Our goal is to anchor high-value activities here, create good jobs for Singaporeans, enhance the resilience and diversity of Singapore’s financial sector, and benefit market participants in Singapore and the region.”

The job-creation vector runs across multiple domains: vaulting and logistics operations requiring highly specialised security and technical skills; trading and relationship management roles that would see Singapore-based professionals managing bullion flows across the region; research and analysis functions supporting pricing, risk management, and market intelligence; and compliance and regulatory roles as the ecosystem scales. Each segment represents high-value employment that aligns with Singapore’s broader strategic objective of moving up the economic value chain.

There is also a financial-sector resilience argument. Singapore’s economy is uniquely exposed to global trade flows and financial-market volatility. A thriving gold ecosystem — which tends to perform precisely when other financial assets are under stress — would provide a countercyclical buffer for the city-state’s economy, reducing correlated risk across its financial-services sector. Gold’s demonstrated capacity to retain value during periods of geopolitical turbulence, dollar weakness, and financial-market dislocation makes it an attractive addition to Singapore’s financial product mix.

The tax revenue implications are harder to quantify but potentially significant. Singapore’s zero-GST treatment of investment-grade precious metals already attracts substantial bullion import and export activity. A deeper ecosystem — one that includes clearing, settlement, central-bank custody, and listed derivatives — would generate substantial transactional and corporate tax flows, as well as income from the highly paid professionals it attracts.

Risks and Challenges: The Road From Ambition to Infrastructure

Intellectual honesty requires acknowledging the headwinds. Building a genuine Asia gold trading liquidity 2026 hub is not a matter of announcing working groups and waiting for the market to arrive. London’s primacy is self-reinforcing: it commands the deepest liquidity pool precisely because the deepest liquidity pool is already there. Persuading traders, banks, and institutional investors to shift settlement and pricing activity to Singapore requires a critical-mass threshold that is genuinely difficult to reach.

The MAS SBMA gold market development working group has wisely sequenced its ambitions — beginning with infrastructure and standards before capital-market products, and with an explicit acknowledgment that implementation details will take months to finalise. This is prudent. Rushed infrastructure in gold markets creates precisely the kind of settlement uncertainty that drives sophisticated clients back to established hubs.

Regulatory alignment with LBMA standards, in particular, requires careful bilateral engagement. The LBMA’s accreditation processes for Good Delivery refiners and vault operators are rigorous and time-consuming. Singapore will need to demonstrate that its standards are not merely internationally “aligned” but genuinely interoperable — that a bar vaulted in Singapore can move seamlessly into and out of the London market without friction.

The geopolitical environment, while providing the tailwind for gold demand, also creates complexity. Central banks remained firm buyers of gold in 2026, even as prices were skyrocketing to records in January, though the institutions’ appetite for bullion could face a stern test amid rising geopolitical tensions in the Middle East. A prolonged conflict that pushes energy prices materially higher could sustain inflationary pressures that complicate interest-rate trajectories — creating short-term headwinds for gold prices even as structural demand remains intact. Singapore’s hub ambitions are a decade-long project; short-term price volatility is noise.

Finally, there is the challenge of liquidity chicken-and-egg dynamics. Derivatives markets need market-makers; market-makers need volume; volume requires end-users; end-users require liquidity. Breaking this circularity requires either regulatory mandates (which MAS has historically been reluctant to impose) or creative commercial incentives that bring anchor market-makers into the ecosystem early. The presence of JPMorgan Chase and UBS in the working group suggests that tier-one international banks are prepared to play this role — but their commitment to active market-making in Singapore-listed gold products remains to be demonstrated in practice.

What This Means for Global Investors and the Future of Asian Finance

For institutional investors and family offices, Singapore’s gold-hub initiative is worth watching closely for two reasons. First, the Singapore gold-related capital market products that emerge from the working group will create new instruments for accessing Asian gold markets — potentially including ETFs, forwards, and structured notes that offer superior cost and settlement efficiency compared to routing through London or New York. Second, and more broadly, Singapore’s emergence as a MAS gold vaulting centre for sovereign entities signals a structural shift in where the world’s financial infrastructure is being built.

The city-state’s strategic gambit is fundamentally a bet on three durable trends: the continuing shift of economic weight to Asia, the sustained de-dollarisation impulse among emerging-market central banks, and the structural demand for gold as a hedge against geopolitical entropy. All three trends have powerful momentum and are unlikely to reverse in the medium term.

Turning Singapore into what one might call the Zurich of the East — a politically neutral, impeccably regulated custodian of global wealth, positioned at the intersection of the world’s most dynamic economic geography — would represent one of the most consequential feats of financial statecraft in Asia’s modern economic history. The working group’s mandate runs through 2026, with periodic implementation updates promised. By year-end, the contours of Singapore’s new gold architecture should be clear.

Gold, after all, has always been less about the metal itself than about the institutions trusted to hold it. Singapore, on March 27, 2026, announced its candidacy for that trust at a regional scale. The audition has begun.

Discover more from The Monitor

Subscribe to get the latest posts sent to your email.

Millions of Burmese Struggle to Find Safety in Thailand

What Is the No Kings Protest? Inside Minnesota’s Historic 2026 Flagship Rally Against Authoritarianism

OPINION | Global South Peace Efforts: How the World’s New Mediators Are Reshaping Diplomacy in 2026

Singapore’s Bold Bid to Become Asia-Pacific’s Gold-Trading Powerhouse: Why the City-State Is Racing to Capture Bullion Liquidity and Central-Bank Vaults

The Private Firms Powering China’s Military AI Push

Trump Extends Iran Talks Deadline amid Sell-Off on Wall Street

Indonesia’s Danantara Shifts to Investment Phase, Targets 7% Returns — Sovereign Wealth Fund Enters Deployment Era Under Prabowo’s Ambitious Vision

AI is dressing up greed as progress on creative rights

Iran’s Tenacious Regime and the Future of the Gulf

Singapore’s Bold Bid to Become Asia-Pacific’s Gold-Trading Powerhouse: Why the City-State Is Racing to Capture Bullion Liquidity and Central-Bank Vaults

Qatar warns Middle East war will force Gulf to stop energy exports within days

OPINION | Global South Peace Efforts: How the World’s New Mediators Are Reshaping Diplomacy in 2026

Four Killed in Beirut Hotel Strike, Israel Says It Targeted Iranian Commanders

The Hormuz Crisis: How US-Iran War Is Reshaping Gulf Geopolitics and Global Energy Security

Iran’s Tenacious Regime and the Future of the Gulf

Indonesia’s Danantara Shifts to Investment Phase, Targets 7% Returns — Sovereign Wealth Fund Enters Deployment Era Under Prabowo’s Ambitious Vision

Brent Crosses $100 as Indian Tanker Path Corrected Near Strait of Hormuz

The 400 Million Barrel Question: Can the IEA’s Historic Reserve Release Save the Global Economy from Iran’s Energy War?

-

Featured5 years ago

Featured5 years agoThe Right-Wing Politics in United States & The Capitol Hill Mayhem

-

News4 years ago

News4 years agoPrioritizing health & education most effective way to improve socio-economic status: President

-

China5 years ago

China5 years agoCoronavirus Pandemic and Global Response

-

Canada5 years ago

Canada5 years agoSocio-Economic Implications of Canadian Border Closure With U.S

-

Democracy5 years ago

Democracy5 years agoMissing You! SPSC

-

Conflict5 years ago

Conflict5 years agoKashmir Lockdown, UNGA & Thereafter

-

Democracy5 years ago

President Dr Arif Alvi Confers Civil Awards on Independence Day

-

Digital5 years ago

Digital5 years agoPakistan Moves Closer to Train One Million Youth with Digital Skills